Introduction

Private debt (private credit) has evolved from a niche alternative to a core allocation for institutional investors, with the US market estimated at roughly $1.5 trillion by 2024. This article synthesizes market-size projections through 2029, analyzes performance and allocation trends, describes structural and technological innovations, and evaluates the principal risks and controversies that will shape the next phase of private debt’s integration into mainstream finance. Key SEO terms such as "private debt market," "private credit investments," and "direct lending" are incorporated throughout to support discoverability for institutional investors and analysts.

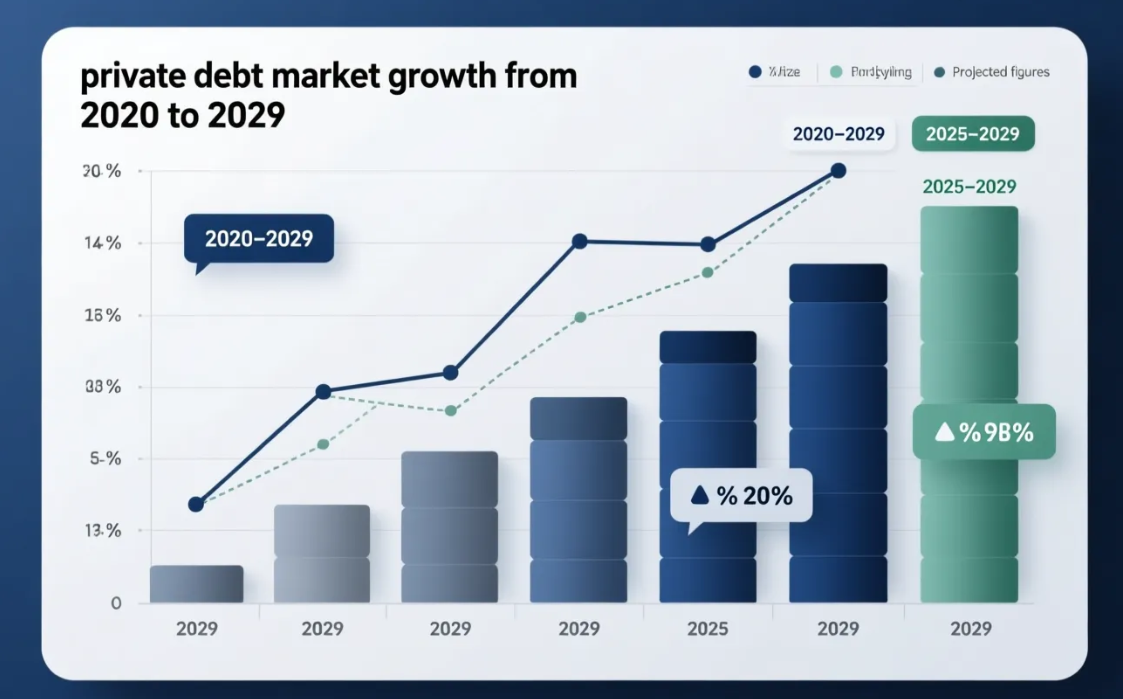

1. Market Growth Trajectory and Size Projections (2025-2029)

The US private debt market has expanded rapidly over the past decade as banks retrenched from certain segments of lending and institutional investors sought yield in a low-rate environment. By many estimates, AUM for private credit in the United States ranged between $1.2 trillion and $1.7 trillion in 2024, with commonly cited industry sources including Preqin, PitchBook, and S&P Global documenting substantial flows into direct lending, specialty finance, and opportunistic credit strategies.

Historical growth has been driven by regulatory changes (higher bank capital requirements under Basel III/IV and post-crisis reforms), fee-seeking behavior by asset managers, and strong institutional demand for uncorrelated income. Consensus CAGR estimates for private credit AUM over recent years generally fall in the 15–20% range, reflecting both strong net inflows and fundraising momentum across strategies.

Current strategy breakdowns show direct lending as the largest component of private debt, followed by distressed and special situations, mezzanine, and specialty finance. Middle-market lending—loans to companies with EBITDA typically between $10 million and $100 million—remains the most active origination channel for private credit managers.

After the first key data point above, the projected market trajectory to 2029 is robust. Most industry outlooks place US private credit AUM in the range of $2.2 trillion to $2.5 trillion by 2029, assuming continued institutional allocations and moderated macro volatility. These projections reflect both organic growth of existing managers and scaling of new strategies, plus geographic expansion in APAC and Europe that fuels cross-border product development.

Sector-specific growth expectations are meaningful: direct lending is expected to remain the largest share of AUM, while distressed and special-situations strategies typically expand during dislocations. Specialty finance—covering consumer installment, equipment finance, and asset-backed private credit—has also shown durable investor interest as managers apply credit expertise to underbanked niches.

| Metric | 2024 Estimate | 2029 Projection | Sources |

|---|---|---|---|

| US Private Credit AUM | $1.2T–$1.7T | $2.2T–$2.5T | Preqin, PitchBook |

| Typical CAGR (recent years) | — | 15%–20% | BIS, Preqin |

| Core strategy IRR / yields | 8%–12% (direct lending) | — | Cambridge Associates, PitchBook |

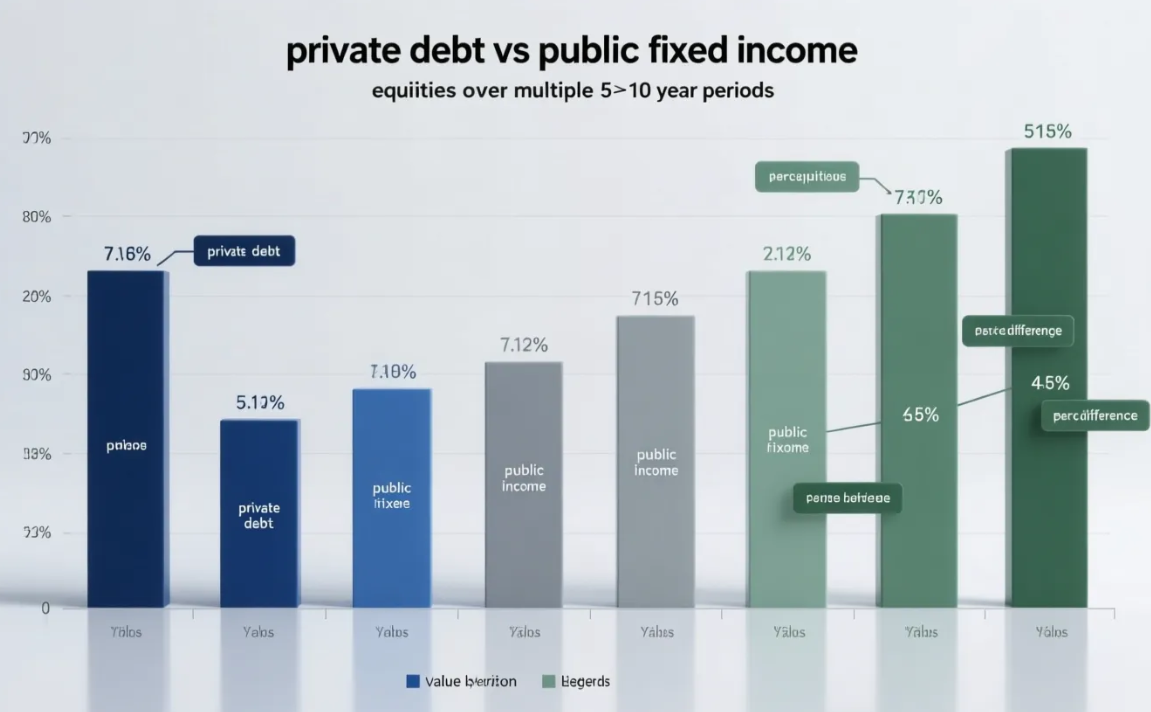

2. Key Performance Metrics and Investment Trends Analysis

Performance characteristics vary by sub-strategy but share common themes: contractual cash yields above similarly rated public bonds, lower historical volatility versus equities, and limited public-market correlation. Core direct lending strategies have historically targeted net internal rates of return (IRRs) in the mid-to-high single digits or low double digits—commonly referenced ranges are 8–12% net—depending on leverage, origination terms, and realized credit outcomes.

Yield spreads over benchmarks (e.g., senior secured loan indices or comparable corporate bond spreads) reflect illiquidity premia, structural protections (seniority, covenants, collateral), and manager value-add in underwriting. Default and recovery dynamics are strategy-dependent: resilient underwriting and senior-secured positions have produced relatively high recoveries in many middle-market transactions, while opportunistic and mezzanine strategies exhibit higher variance.

Institutional allocation trends show pronounced growth among public pension funds, insurance companies, and defined-contribution-like entities that pursue private credit via separate accounts or commingled funds. Family offices and high-net-worth investors are increasing participation through feeder vehicles and registered fund wrappers that expand access beyond traditional institutional capital.

Dry powder (un-deployed committed capital) remains elevated at many managers but has been progressively deployed as new deal flow and sponsor financing needs persist. Deployment pace is a key metric for future return realization; extended high levels of dry powder can compress returns if competition drives looser terms.

Emerging thematic opportunities also influence performance expectations. ESG-linked lending structures—where financing terms are tied to sustainability targets—are increasingly common, and managers are building frameworks for ESG monitoring. Technology and fintech credit (including lending to fintech balance sheets) and infrastructure-related private credit are other areas showing differentiated return profiles and structural protections that can appeal to liability-aware investors.

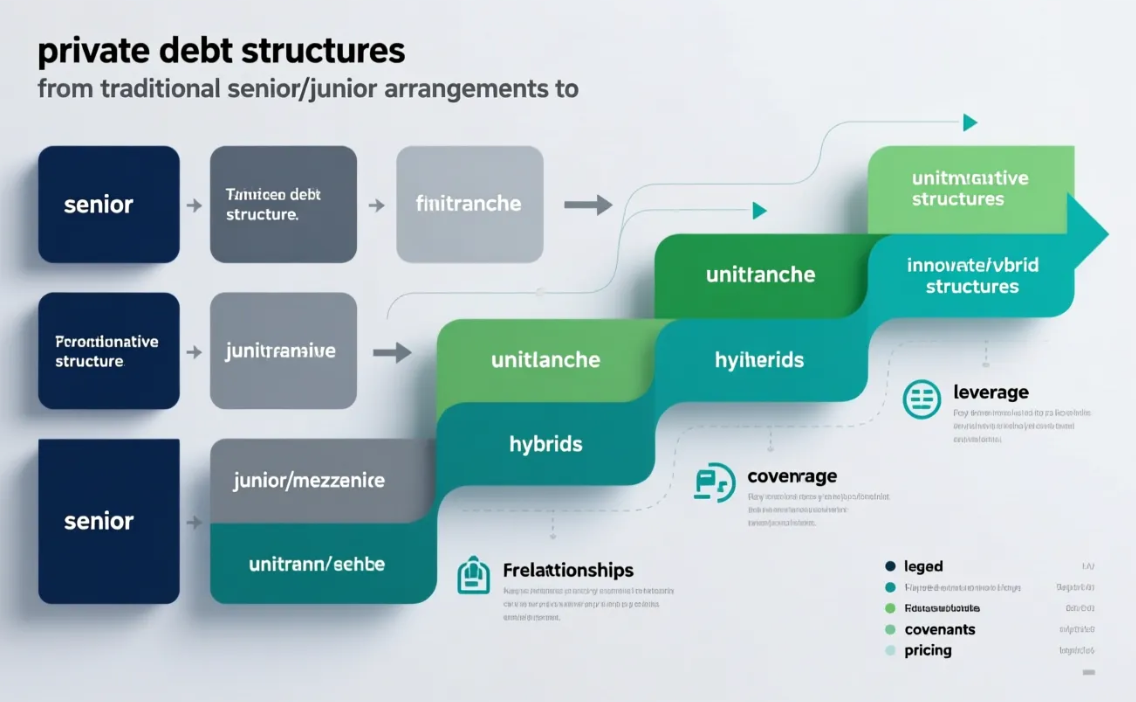

3. Structural Innovations and Product Development in Private Credit

The private credit industry is innovating on multiple fronts: transaction structures, documentation, distribution, and technology. The evolution from traditional senior/junior stacks to unitranche and hybrid solutions reflects borrower demand for simplified capital structures and lender appetite for tailored risk-return configurations. Unitranche loans—combining senior and subordinate economics into a single instrument—remain widespread in middle-market direct lending, offering streamlined execution at the cost of inter-lender subordination layering.

Other documentation trends include the gradual prevalence of covenant-lite facilities in certain sponsor-backed segments, and flexible amendment provisions designed to balance creditor protections with borrower operational flexibility. These developments require careful covenant-by-covenant analysis; the implied trade-off between pricing, covenants, and liquidity terms is central to manager selection and portfolio construction.

Technology is transforming underwriting, servicing, and secondary-market functionality for private credit. Managers increasingly deploy artificial intelligence and machine learning models to enhance credit origination and monitoring, using alternative datasets (transactional, supply-chain, point-of-sale) to improve risk assessment. Blockchain and distributed-ledger technologies are being piloted for loan syndication, ownership registry, and operational reconciliation, promising efficiency gains though still facing legal and regulatory hurdles.

Product innovation also targets investor access and liquidity. Continuation vehicles and dedicated secondaries offerings allow managers and limited partners to match time horizons and provide exit pathways. Registered retail-accessible private credit funds and interval funds have broadened the investor base, although they introduce additional regulatory and liquidity-management considerations. Cross-border and multi-currency lending platforms are enabling managers to deploy capital into international opportunities while managing FX and regulatory complexities.

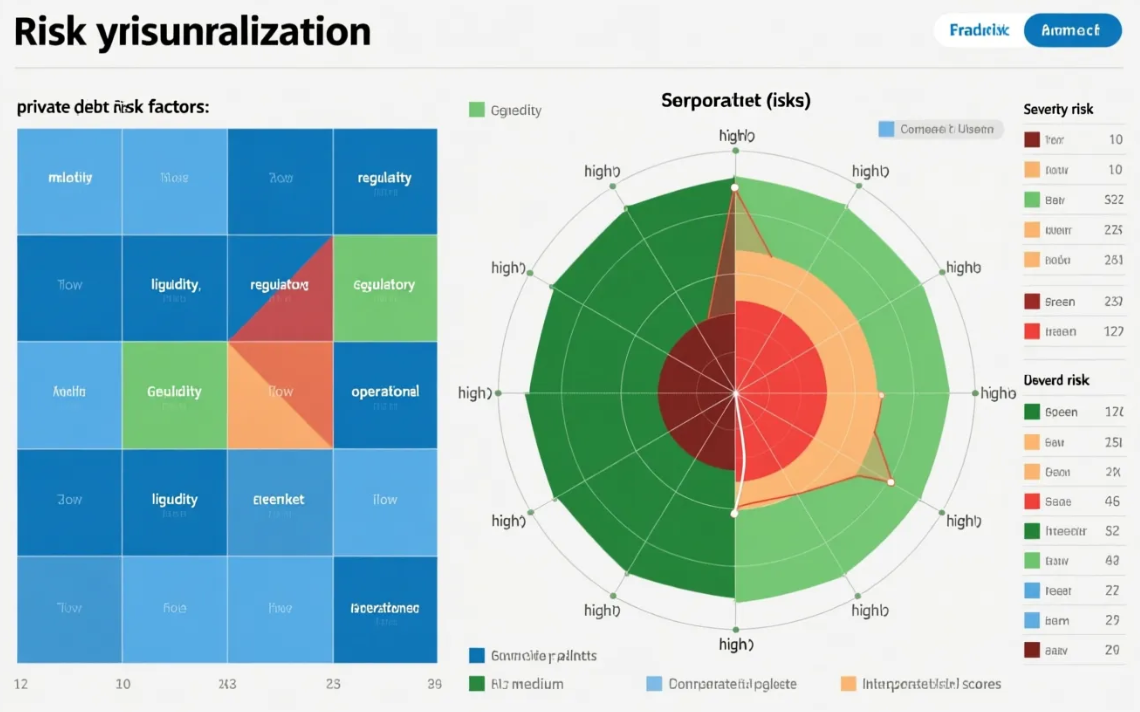

4. Risk Assessment and Market Controversies Evaluation

Credit and liquidity risk are the most immediate concerns for private credit investors as the macroeconomic environment evolves. Private loans often carry interest-rate sensitivity (through floating-rate coupons or repricing features) but can embody duration risks in covenanted cash flows, particularly in longer-tenor structures. Stress-testing and recession-scenario analysis are essential: a downturn that raises default incidence materially will test recovery assumptions and manager workout capabilities.

Liquidity mismatch is another critical risk for closed-end or semi-liquid structures. Investor redemptions, mark-to-market pressures, and delayed realizations can produce valuation volatility. Managers employ gate mechanisms, side pockets, and staggered liquidity windows to manage these mismatches, but these tools can also constrain investor access in stressed market periods.

Regulatory and compliance pressures are intensifying as private credit scales. Cross-border activity raises questions about regulatory arbitrage, and evolving rules on fund transparency, reporting, and systemic risk monitoring (by regulators such as the SEC and international bodies) may increase operational costs for managers. Anti-money-laundering (AML) and KYC expectations are likewise rising for lenders that source deals in multiple jurisdictions.

Market controversies have centered on transparency, valuation practices, and aggressive lender conduct. Debates about private asset valuation methodologies—particularly around illiquid instruments with limited observable comparables—are ongoing, with calls from some public pension and regulatory stakeholders for standardized reporting. Incidents of aggressive creditor behavior or controversial workout tactics toward stressed borrowers have prompted reputational scrutiny, emphasizing the need for robust governance and stewardship in private credit underwriting.

Conclusion

Private debt in the United States has moved from the margins to the center of institutional portfolios, driven by yield-seeking behavior, regulatory shifts in the banking sector, and product innovation. With AUM estimated near $1.5 trillion in 2024 and many forecasts projecting $2.2–$2.5 trillion by 2029, the asset class will continue to exert substantial influence on capital markets.

Investors considering private credit should prioritize manager selection, rigorous underwriting frameworks, transparent valuation practices, and stress-tested liquidity solutions. The convergence of private and public credit markets—facilitated by technology, enhanced disclosure, and secondary-market development—will improve scalability but also attract greater regulatory and public scrutiny.

Ultimately, private debt’s transition from alternative to mainstream hinges on its ability to deliver durable risk-adjusted returns while managing the structural, operational, and ethical challenges that accompany scale. For institutional investors, private credit offers meaningful diversification and income potential, but it requires sophisticated governance and active oversight to navigate the next chapter of growth and innovation.

Selected sources: Preqin, PitchBook, S&P Global, Cambridge Associates, BIS, Cerulli Associates (links embedded above).