Introduction

The rapid escalation in average smartphone prices over the past half-decade has made mobile phone installment plans a routine part of device purchases for many U.S. consumers. Smartphone financing—from carrier-managed 24-to-36-month plans to manufacturer-promoted programs and a growing array of buy-now-pay-later (BNPL) options—now represents a significant share of device distribution and, consequently, consumer financial exposure. This article synthesizes market trends, compares provider models, summarizes regulatory scrutiny and consumer-protection issues, and examines the economic tensions that shape how Americans buy and keep their phones.

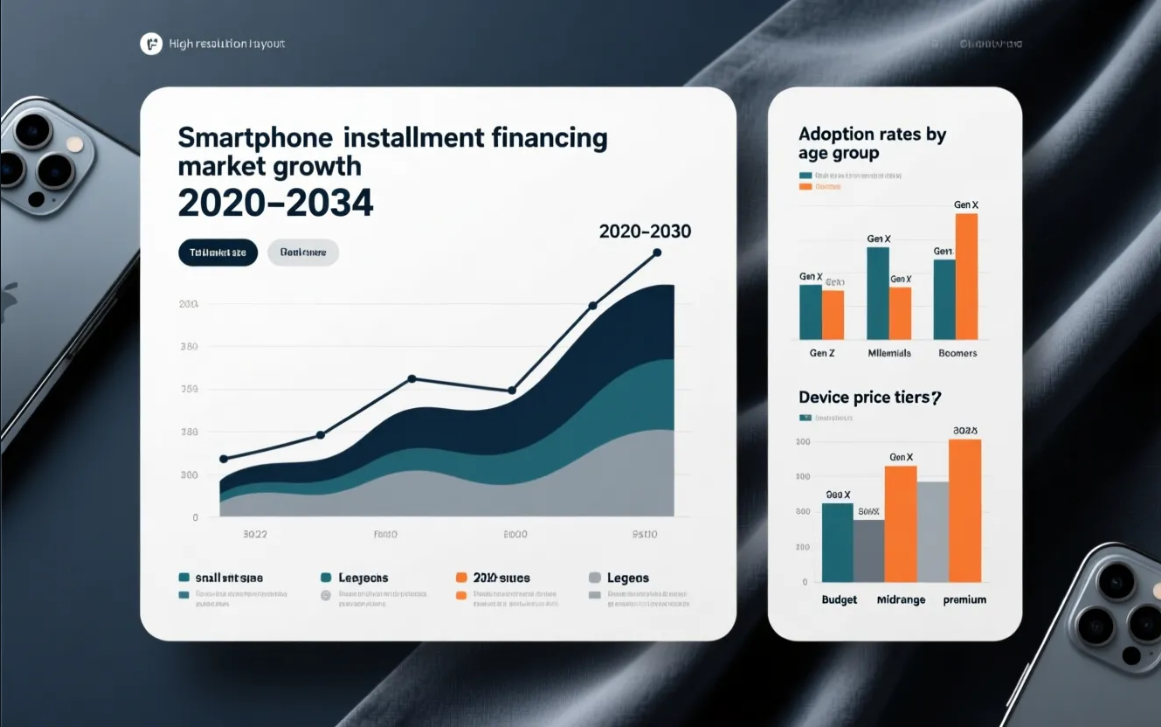

1. Market Size Analysis and Growth Trends of Smartphone Installment Financing in the U.S.

1.1 Definition and Scope

"Smartphone installment financing" encompasses any arrangement allowing a consumer to pay for a mobile handset across multiple scheduled payments. This includes plans embedded in a carrier bill, offers from manufacturers, financing through third-party BNPL vendors, and loans from banks or credit products. Adoption has grown in tandem with rising flagship device average selling prices (ASPs), as financing has become a standard sales tool.

1.2 Current Market Valuation and Projected Growth Rates

Industry research through mid-2024 indicates that a substantial and rising fraction of U.S. device transactions are funded via installment or consumer-credit structures. Estimates from market analysts and industry reports generally place financed device penetration in the range of 30–50% of handset sales for major channels during 2021–2024, with premium tiers showing the highest incidence of financing. Projections to 2030 anticipate continued growth, driven by subscription models, deeper BNPL penetration, and carrier trade-in ecosystems. Analysts commonly project mid-single-digit to low-double-digit compound annual growth rates (CAGR) for financed device volumes, although figures vary by source (see industry sources such as Counterpoint Research, IDC, and Statista for vendor-specific estimates).

1.3 Demographic Trends Driving Adoption

Financing adoption skews notably by age and income:

-

Younger buyers (18–34) are more likely to use carrier installment plans and BNPL, prioritizing convenience and lower perceived short-term cost.

-

Middle-aged buyers (35–54) utilize a mix of carrier, bank, and credit card financing.

-

Lower-to-moderate income households rely on installments to spread upfront costs.

-

Higher-income consumers often use financing for cash-flow management or to access premium devices without liquidating savings.

-

Geographically, urban and suburban regions show higher financing rates, driven by concentrated marketing incentives and device upgrade cycles.

1.4 Impact of Premium Smartphone Pricing on Financing Demand

Average flagship prices rose materially from 2018 to 2024, pushing many consumers toward multi-month payment plans rather than outright purchase. Financing penetration is highest in the flagship and premium tiers: devices priced above $800 typically see financing rates significantly above average compared with budget devices under $400. Consumer willingness to finance correlates strongly with perceived device value, the availability of carrier subsidies or trade-in credits, and attractive promotional terms (e.g., zero-interest or deferred payment offers).

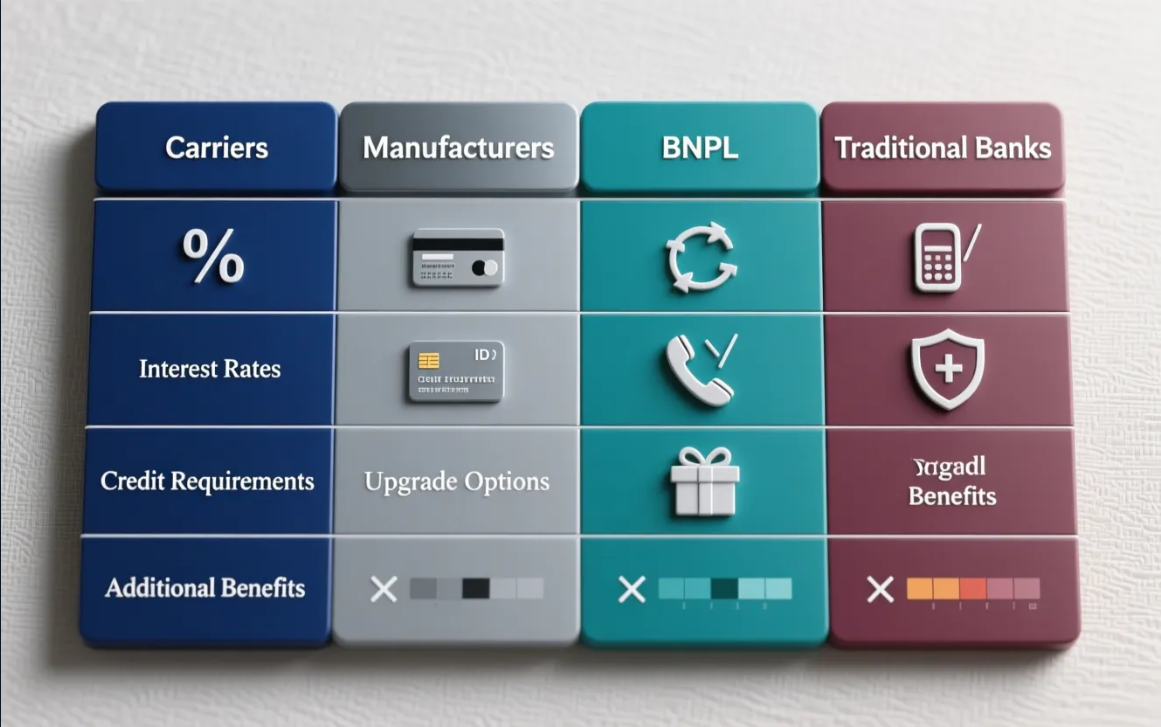

2. Comparative Landscape: Carriers vs. Manufacturers vs. BNPL vs. Traditional Banks

2.1 Overview

The provider landscape is heterogeneous. Four dominant models operate in the U.S. market: carrier-led financing, manufacturer-direct programs, third-party BNPL, and traditional bank/credit alternatives. Each model features distinct underwriting, pricing, and consumer experience characteristics.

| Feature | Carriers | Manufacturers | BNPL Providers | Traditional Banks/Credit Cards |

|---|---|---|---|---|

| Primary Channel | Retail stores, carrier websites | Brand websites, retail partners | Online checkout partners, in-store integrations | Banks, card issuers, personal loans |

| Interest & Fees | Often 0% promotional plans; late fees & service bundling common | Often 0% for set terms; bundled service perks | Variable: some 0% short-term offers; deferred-interest or late fees possible | Interest-bearing credit lines or loans; APR varies |

| Credit Checks | Soft or hard inquiries depending on plan | Varies; often soft checks for promotional plans | Range from soft checks to no-check micro-approval for small amounts | Standard credit underwriting |

| Upgrade & Trade-in | Robust early-upgrade and trade-in programs | Tight integration with trade-in and warranty services | Less focus on upgrade programs; some partnerships exist | Not typically focused on upgrades; cash-out options available |

| Additional Benefits | Bundled service discounts, loyalty incentives | Warranty, device care bundles, loyalty incentives | Flexible payment scheduling, quick approval | Consolidation of payments, rewards on some cards |

2.2 Carrier Financing Models and Advantages

Carriers (e.g., Verizon, AT&T, T-Mobile) combine installment payments with service contracts and trade-in credits, enabling marketing of "$0 down" promotions and early-upgrade options. Their vertical integration—billing device payments alongside service—simplifies collections and supports long-term customer retention. However, carriers may embed conditions—such as early-upgrade requirements, handset unlocking rules, or billing entanglements—that consumers should carefully review.

2.3 Manufacturer Financing Programs and Ecosystem Benefits

Brands like Apple and Samsung offer direct financing with several advantages: seamless integration with device warranties, device-care plans, and loyalty/upgrade pathways. Manufacturer plans often present straightforward promotional terms for flagship models and can reduce friction at purchase. However, they may require purchases through specific retail channels or enrollment in associated programs (e.g., Apple Card).

2.4 BNPL Providers Disrupting Traditional Financing

BNPL entrants (Affirm, Klarna, PayPal Pay Later, and others) increasingly support device purchases through both online and some in-store partnerships. BNPL can provide short-term, no-interest options or stretched multi-month plans. Their fast approval and consumer-facing transparency are appealing. However, some BNPL offers include deferred-interest features or high late fees and can complicate consumers' credit exposure if multiple plans are opened across different vendors.

2.5 Traditional Bank Financing and Credit Card Alternatives

Personal loans, installment loans, or credit-card financing remain options for consumers who prioritize credit-line consolidation or rewards. These products typically involve established underwriting and standard APRs. They may be appropriate for consumers with existing credit relationships who prefer to manage payments outside carrier or manufacturer billing systems.

3. Regulatory Scrutiny and Consumer Protection in Device Financing Practices

3.1 Regulatory Landscape Overview

Device financing sits at the intersection of consumer credit regulation, telecommunications rules, and emerging BNPL oversight. Key U.S. oversight actors include:

-

The Consumer Financial Protection Bureau (CFPB) , focusing on fair lending and disclosure.

-

The Federal Trade Commission (FTC) , policing deceptive practices.

-

The Federal Communications Commission (FCC) , addressing telecom-specific issues like handset unlocking.

-

State Attorneys General, who enforce state-level consumer protection laws.

3.2 Common Consumer Protection Issues and Complaints

Consumers commonly report concerns including:

-

Unclear or hidden fees.

-

Surprise charges when terminating service early.

-

Misleading promotion terms.

-

Credit reporting disputes when installment plans are misreported or defaulted.

-

Difficulty resolving billing errors.

-

Confusion about device unlocking eligibility.

-

Lack of transparent disclosure for late fees or deferred-interest mechanics.

3.3 Recent Enforcement Actions and Policy Activity

Regulators have increased scrutiny on BNPL and device-financing practices. The CFPB and FTC have issued guidance emphasizing transparency around fees, clear disclosures for consumers, and oversight of "point-of-sale" financing. State Attorney General offices have pursued cases where practices were deemed deceptive or where consumers experienced unfair billing or contract terms. Industry responses include improved disclosures, voluntary codes of conduct, and product adjustments to reduce consumer harm. However, regulatory attention remains active as new product structures continue to emerge.

3.4 Best Practices for Consumer Protection and Transparency

Policy recommendations and consumer-advocacy proposals emphasize:

-

Clear pre-purchase disclosure of total cost.

-

APR-equivalent information where applicable.

-

Explicit terms for early termination or upgrades.

-

Robust mechanisms for dispute resolution.

-

Accurate credit reporting standards.

Consumers benefit when providers offer clear written terms, an easy process for returns and repairs, and accessible channels to dispute billing or credit-report issues promptly.

4. Economic Tensions: Device Pricing, Lifecycle Extension, and Consumer Affordability

4.1 The Rising Cost of Premium Smartphones and Financing Necessity

Higher ASPs for flagship phones have shifted more consumers into financing arrangements, making affordability a central concern. Financing can lower the barrier to entry, but it may also extend consumer obligations over months or years and increase cumulative outlays when fees or early-exit penalties apply. Evaluating the total cost of ownership is therefore essential.

4.2 Device Lifecycle Extension vs. Upgrade Cycle Pressures

Manufacturers and carriers incentivize frequent upgrades—through trade-in credits, limited-time promotions, or early-upgrade programs—while environmental and consumer-affordability arguments favor extending device lifecycles. Longer-lived devices reduce household spending pressures and environmental impact, but the ecosystem's commercial incentives often prioritize turnover. This tension plays out in financing design: upgrade-friendly plans encourage repeated financed purchases, while subscription or device-as-a-service (DaaS) models emphasize lifecycle management and potential refurbishment streams.

4.3 Affordability Challenges and Payment Burden Analysis

Monthly payment burdens vary by plan term and device price. A flagship device on a 24–36 month plan can produce monthly obligations that compete with other recurring household costs. For households financing multiple devices or carrying legacy plans, cumulative monthly obligations can increase delinquency risk. Data from consumer credit and payments studies indicate that payment stress concentrates among lower-income cohorts and younger consumers who use multiple credit products simultaneously.

4.4 Future Trends: Subscription Models and Circular-Economy Integration

Looking ahead, industry trends include the growth of subscription-style device offerings (Device-as-a-Service), expanded refurbishment and certified-preowned channels, and financing products designed specifically for refurbished phones. These models can reduce upfront costs and environmental impact while enabling manufacturers and carriers to retain revenue through ongoing service relationships. If executed with transparent pricing and strong consumer protections, these business models may ease affordability pressures while encouraging longer device lifecycles.

5. Consumer Guidance: Choosing the Right Financing Option

-

Assess total cost, not just the monthly payment: Calculate the aggregate price paid over the term—include any fees, taxes, and potential trade-in conditions. A low monthly payment with a large final balloon payment or high early termination fee can be more expensive overall.

-

Understand credit and reporting implications: Confirm whether the financing results in hard credit inquiries, what is reported to credit bureaus, and how missed payments will be recorded. BNPL providers differ: some do not report routinely, while others may report missed payments and affect credit indirectly through collections.

-

Prioritize transparent terms and dispute channels: Choose providers that supply clear written agreements and easy-to-access customer service for billing disputes, device repairs, and warranty claims.

-

Consider refurbished or DaaS options: If affordability is the primary constraint, certified refurbished devices or subscription models can reduce upfront cost and provide warranty-like protections without multi-year purchase obligations.

6. Industry Outlook and Implications

Competition and product innovation will continue to drive diverse financing models. Carriers and manufacturers will refine upgrade and loyalty incentives, while BNPL and fintech entrants will push for simpler checkout experiences. Regulators are likely to expand scrutiny—particularly around disclosure and consumer protection—which will shape product design and fee structures. A greater emphasis on circular economy solutions and certified-refurbished channels may reshape device supply economics and, over time, reduce financing volumes for new flagship models.

7. Conclusion

Smartphone installment plans have materially expanded consumer access to higher-priced devices, but they also introduce financial complexity and exposure. Consumers and advisors should evaluate the full cost of financing, understand reporting and dispute mechanisms, and consider alternative models such as refurbished devices or subscription services when affordability is a concern. For industry stakeholders, balancing accessibility with transparent, consumer-friendly terms will be essential: responsible financing that clearly discloses costs, supports dispute resolution, and encourages sustainable device lifecycles can align commercial objectives with consumer financial well-being.

References and Further Reading

-

Industry market reports: Counterpoint Research, IDC, Statista.

-

Regulatory guidance and statements: Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC).

-

Carrier and manufacturer financing terms: Available on company websites (e.g., Verizon, AT&T, T-Mobile, Apple, Samsung).

-

For regulatory updates and enforcement actions, see the CFPB (https://www.consumerfinance.gov) and FTC (https://www.ftc.gov) press pages.